The issue of a foreign currency shortage, in particular the US currency — and a seemingly looming foreign currency crisis — has been one of the predominant topical issues appearing in the press recently. In this article, I will examine in a robust manner the real problem at hand regarding this matter.

We saw that a few concerns were raised in the press by some sections of the private sector: that the commercial banks are claiming a shortage of foreign currency, and as a consequence, customers are placed on a waiting list to effect payments to suppliers abroad; and likewise for incoming transfers from abroad.

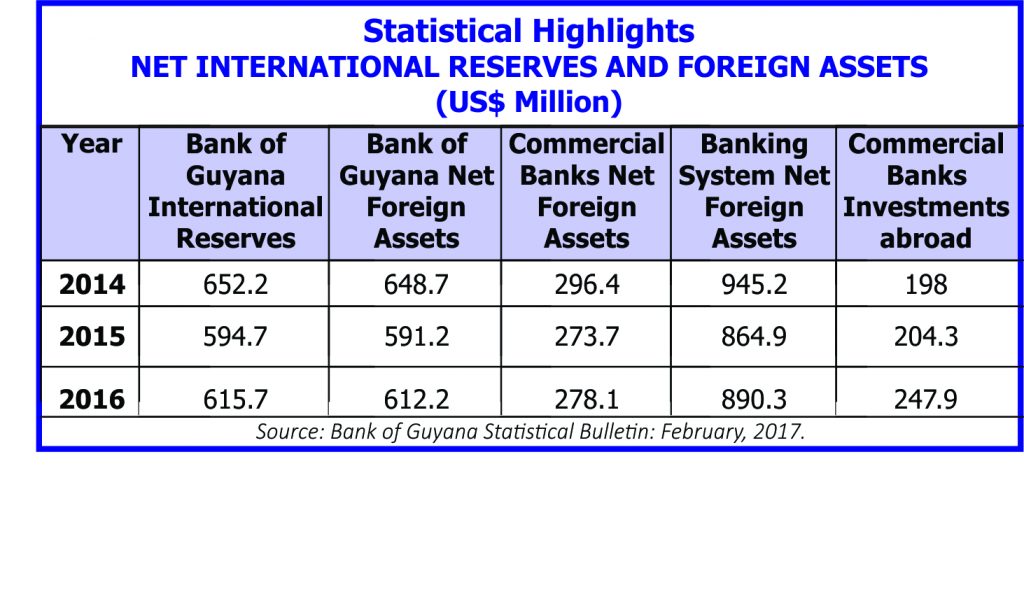

Subsequently, the central bank governor and the minister of finance quickly refuted these claims, and attempted to provide evidence that such a shortage is non-existent by illustrating the level of foreign currency reserves held by the central bank and commercial banks, both locally and abroad; which the governor contended are sufficient and the dollar should not depreciate significantly.

The figures below were extracted from the Bank of Guyana’s Statistical Bulletin report for the years 2015 and 2016. I will examine in some detail the trends reflected in the movements of foreign currency holdings and reserves by the banking system, and its implications on the exchange rate.

Table 1 reveals net foreign assets held by commercial banks increased by USM, or 1.6 percent, in 2016, in comparison to a decrease in 2015 by US .7M; while a marginal increase was recorded in 2016, the composition of commercial banks’ net foreign holdings evidently changed quite significantly. Commercial banks’ investment in foreign markets in 2015 was recorded at 4.3M, reflecting an increase in foreign investments of US.3M, or 3.1 percent. In 2016 however, commercial banks increased their level of foreign investments by a whopping US.6M, or 21.3 percent. This level of increase in foreign investments in effect reduced the availability of foreign currency held by commercial banks to accommodate international trade emanating in the domestic market.

Table 2 reveals that the net inflow of US dollars decreased by approximately US$1,669M in 2016. At the same time, total imports reduced by US $43.8M in 2016 to US$1,447.8M from US $1,491.6M in 2015. And total exports increased by US$286.5M to US$1,420.9M from US$1,134.4M in 2015. Additionally, balance of payments recorded a trade deficit of US$34.3M in 2016, representing a reduction of US$73.4M from US$107.7M recorded in 2015.

Hence, using an average model of calculation from the abovementioned statistics, we could deduce that the net reduction of available US dollars in the domestic foreign exchange market was set at 21.2 percent. One would recognise that this level of foreign currency depletion correlates with the exchange rate’s upward movement to an average of 9.1 percent. Hence there is a real depreciation of the local currency against the US dollar.

There is evidence that the Guyanese dollar has depreciated against the US currency, and the simple demand-and-supply dynamics can explain this. Of key note, however, one of the main causes for this is the significant increase of foreign investments by the local commercial banks coming down to the latter part of 2016. Albeit, this move is quite logical, as the commercial banks found foreign investments more lucrative at a time when the domestic economy was experiencing a decline in economic activities amidst an unstable political environment.

In next week’s edition, a part two to this article will be featured, in which I will continue this discussion on the foreign currency exchange rate and its implications on the financial sector and the economy.

Discover more from Guyana Times

Subscribe to get the latest posts sent to your email.