Given the structural character of the economy (a small and open economy), it is expected that there will be a high reliance on im-ports for consumption and capital development. In such a situa-tion, the proper administration of the stock of foreign currency is of paramount importance in order to enable the economy to be able to meet the demands for foreign exchange to conduct trade. Therefore, there must be discipline in the use of the country’s foreign currency reserves. What the Guyanese people have seen under this Granger regime is anything but the disciplined use of the country’s foreign currency reserves.

Upon its establishment, one of the primary purposes of the Bank of Guyana was given by one of its statutory mandates, which is to foster “domestic price stability through the promotion of stable credit and exchange rate conditions”. One of the preconditions towards fulfilling this mandate is the maintenance of adequate Import Cover in the economy. What is the Import Cover? It is when the stock of the country’s foreign currency reserves at a point in time are compared with the value of imports of merchan-dise goods over a 12-month period. This ratio basically measures a nation’s ability to pay its foreign currency bills. The international norm is that all countries should have a supply of foreign currency to purchase 3 or more months of imports at any point in time.

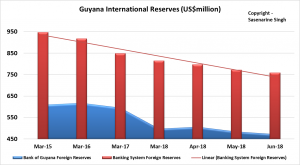

According to the just-released IMF Article IV Report on Guyana for 2017, the gross international reserves (also called foreign cur-rency reserves) were enough to cover 3.2 months of imports at the end of 2017. As the graph below shows, it has been a slip-pery slope for Guyana since March 2015. The empirical evi-dence garnered from the Bank of Guyana Quarterly Report for the first quarter of 2018 revealed that, over the first three months of 2018, this important key performance indicator (KPI) declined to 3.1 months. The Ministry of Finance’s just released Half Year 2018 Report confirms the thread by revealing from its figures that at June 2018, this KPI dropped further to 3.0 months. What message are these figures telling us? Is the Import Cover set to fall below 3 months by Christmas 2018?

As the export sectors continue to not perform at the expected level in 2018 and oil price climbs, the strain on the foreign re-serves will increase. But yet we cannot see the green shoots from the emerging economic sectors that President Granger promised the nation in 2015. All we are getting from Team Granger are lethargy in action and policy paralysis on the in-vestment front. And for good measure, lame excuse after lame excuse.

Based on the trends revealed in the Minister’s Half-Year Report, by the end of 2018, Guyana is expected to have a further deterio-ration in the deficit position on the overall balance of payments. How will Guyana finance this? Well, the Minister was clear in his strategy, his Government plans to further raid the foreign curren-cy reserves at the Bank of Guyana, and he has now given the blanket mandate to the Central Bank to then raid the stock of for-eign currency in the private sector.

This is another clear example of how the Public Sector continues to crowd out the Private Sector upon the arrival of Team Granger. The only outcome of such a dotish strategy is a further deteriora-tion of the exchange rate, which will bring great economic harm to the most vulnerable in Guyana.

The empirical evidence over the period January to June 2018 has revealed that the Bank of Guyana drained US$76.2 million from the local private sector supply of foreign currency to prop-up the stocks in the Central Bank. This is a new but dangerous trend that last happened in the Burnham days, and has started to happen again since 2017. We have a history of what such a strategy can do to the economy.

I am therefore encouraging the authorities to cease and desist from this reckless economic strategy, since it will have long-term consequences for all Guyanese. The foremost consequence is a rapid shortage of foreign currency in the market, which will drive the re-awakening of a parallel foreign exchange market, which can lead to economic retardation. This strategy being used by the Granger Government must be exposed, opposed and reject-ed by the Guyanese people, because all will suffer if it is allowed to continue.

Guyana can do better than this!

Discover more from Guyana Times

Subscribe to get the latest posts sent to your email.